+31 486 820 996

+31 486 820 996 Email

EmailCost management for construction projects is a systematic approach to plan and control resources, cost, profitability and risk throughout the life cycle of a construction project.

Bouwcredits strategic focus is on budgeting, cost planning and procurement to make sure the project meets Client requirements at a reasonable cost level. To do this, we use a uniform framework for measuring, forecasting and reporting of the project costs.

Our objective and reliable estimates or cost reports are the baseline of our advice. We complement this expertise with a solution-aimed attitude to realise project objectives.

‘The goal of Cost Management is to predict the end result!’

For example: a real estate developer may build, maintain, renovate, and then demolish an office building during its lifecycle – at each phase of the building life cycle the developer makes significant investments. To manage these investments, the building developer monitors building operating costs and profitability; evaluates alternative investment opportunities; and initiates, plans and controls improvement projects. These activities are all within the scope of the Cost Management process.

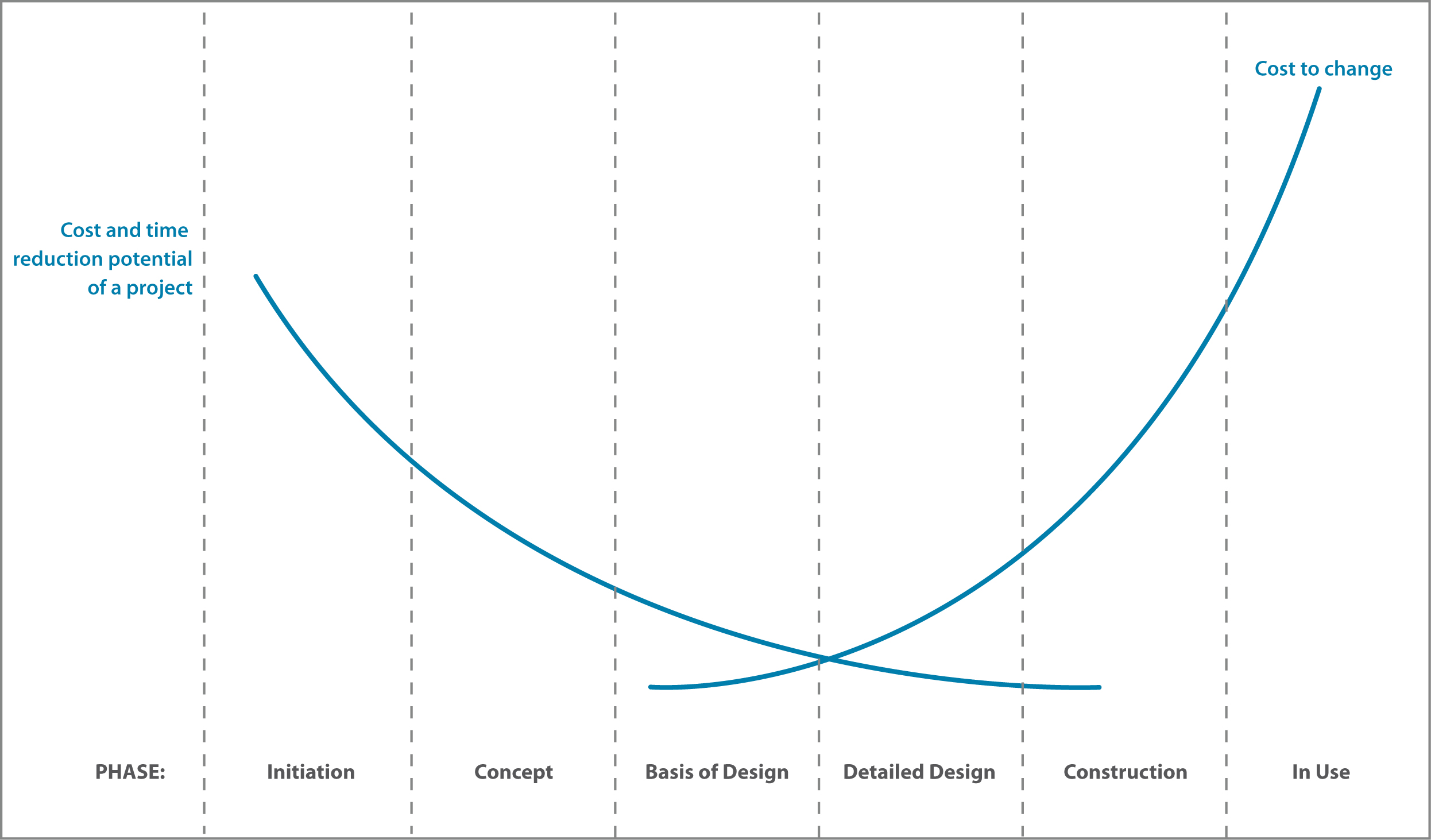

Throughout the entire construction process costs are key to making decisions. During the early stages the potential to influence cost and time is the greatest. The message here is that if changes occur later in the life cycle, the ability to make changes is constrained and the costs of doing so are much higher. This means that, in order to act effectively and to avoid unnecessary costs, early stage scoping & budgeting is vital in realising the optimum project solution.

We understand how complex it is to identify all requirements and costs of the facility at the outset and to make strategic decisions. That is why it is good to involve our Cost Engineer at an early stage.

We understand how complex it is to identify all requirements and costs of the facility at the outset and to make strategic decisions. That is why it is good to involve our Cost Engineer at an early stage.

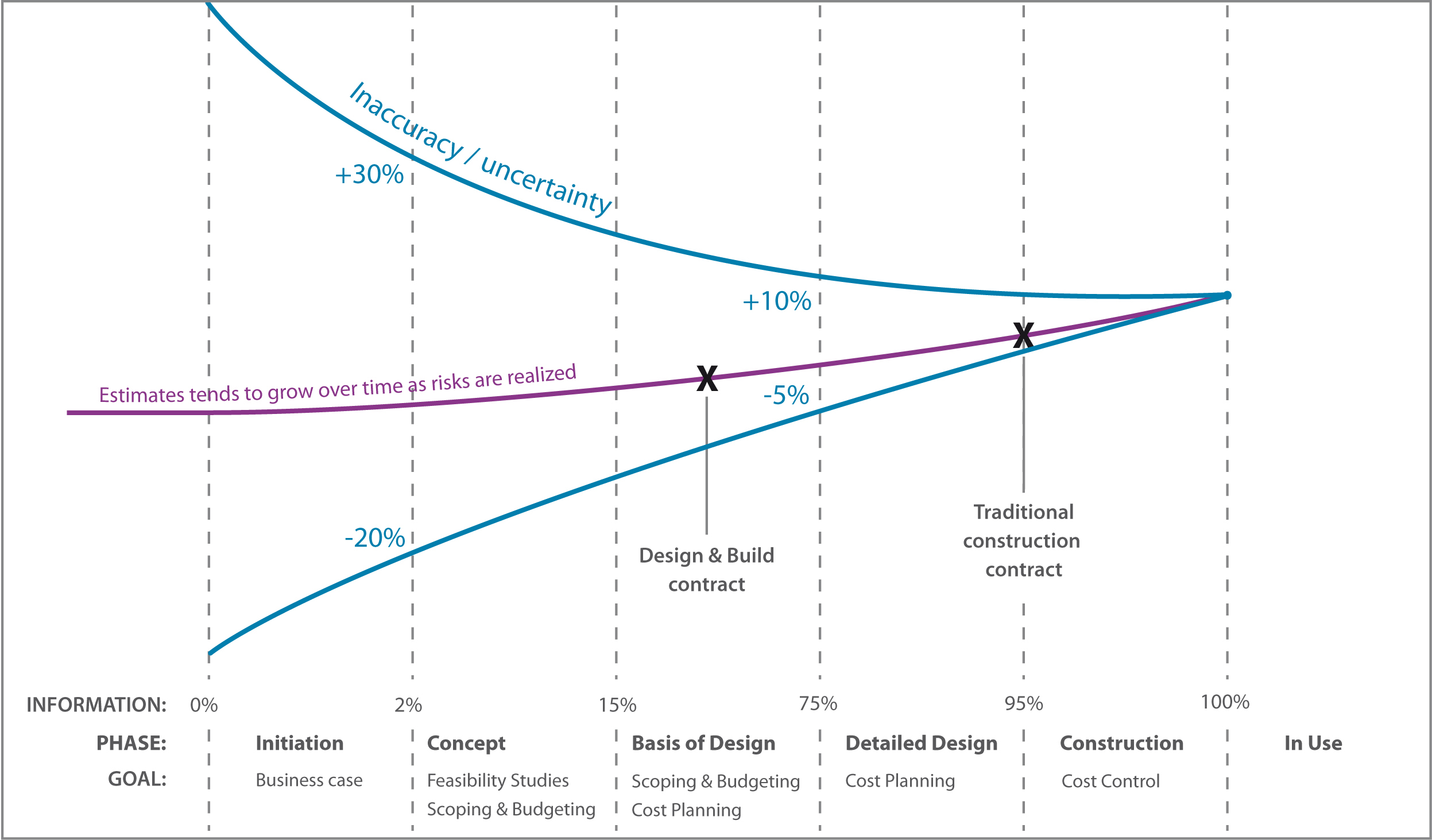

Construction planning typically follows a top-down approach. As the construction process develops more detailed information becomes available. Cost estimates tend to become more accurate as actual circumstances and design progress start to replace the uncertainties and assumptions of the earlier estimates. For example this happens when risks are either mitigated or realised.

These processes are illustrated in the following model.

In addition, narrow risk ranges should be viewed as suspect, because more cost estimates tend to overrun than underrun.

In addition, narrow risk ranges should be viewed as suspect, because more cost estimates tend to overrun than underrun.

Onderzoeken of en hoe uw bouwambitie gerealiseerd kan worden binnen het beschikbare budget.

> Read more

© 2026 Bouwcredits | Trade Register 57611157 | General conditions | Disclaimer